Sustainability Reporting Isn’t Expensive. Inefficiency Is.

For most mid-sized companies, the work required to pull together sustainability information is already happening. It just does not show up as a single effort. It is spread across teams, absorbed into existing roles, and revisited each time a new request comes in. Over time, that effort adds up in ways that are difficult to track but easy to feel. Priorities shift, timelines extend, and teams spend more time assembling information than using it.

Science-Based Targets Are Becoming More Flexible. That Changes What “Credible” Looks Like.

Recent updates to the Science Based Targets initiative introduce a greater degree of flexibility in how emissions reductions are achieved over time. Companies are still expected to meet long-term goals, and minimum levels of ambition remain in place, but the path between the starting point and the endpoint is becoming less rigid.

Are Your Sustainability Efforts Credible?

Across technology, life sciences, and advanced manufacturing, many companies are already doing more on sustainability than they give themselves credit for. They are reducing waste in lab environments, improving energy efficiency in facilities, sourcing materials more thoughtfully, and building products with real-world impact. In ecosystems like thsee, where innovation often moves quickly from lab to market, these efforts are often embedded in how companies operate rather than framed as formal sustainability programs.

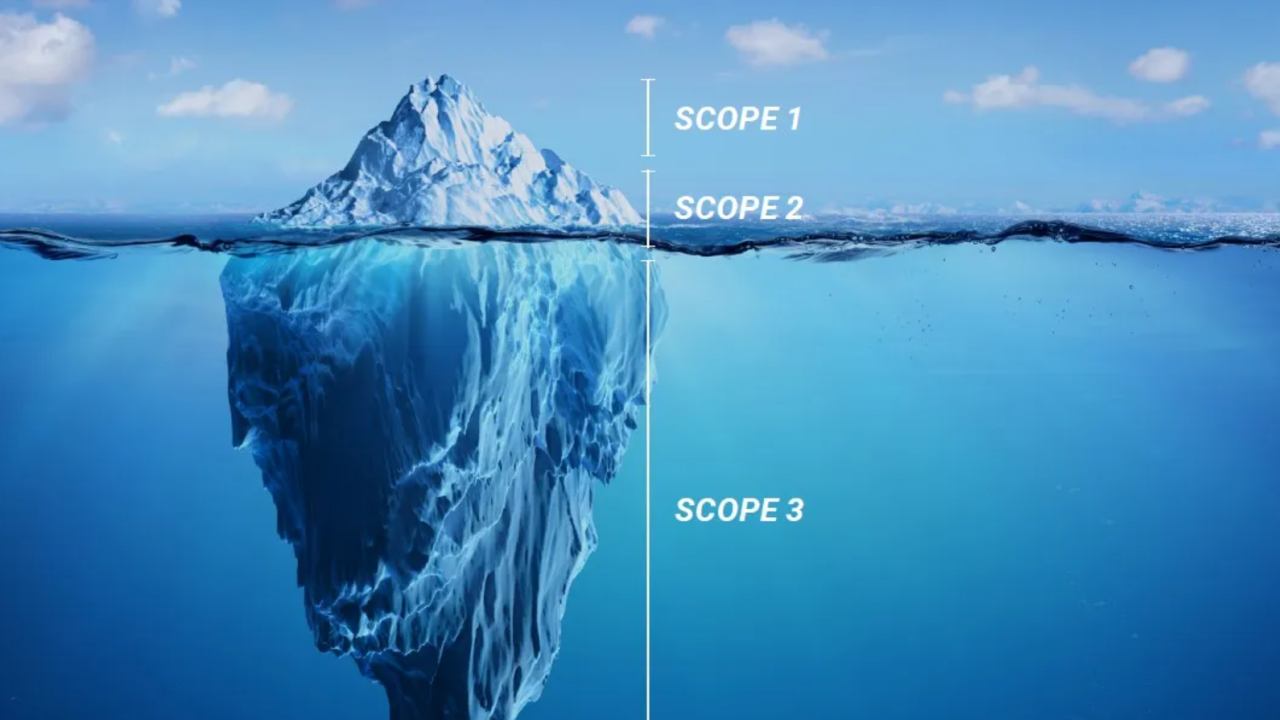

Carbon Accounting Is Potentially Expanding Beyond Emissions

A recent set of developments around insetting and supply chain interventions, including guidance emerging from the AIM platform, points toward a broader shift in how climate impact is defined and reported.

The ESG Puzzle: Complexity Isn’t a Phase. It’s the Environment

Companies are no longer dealing with a single framework or a defined set of expectations. They are operating across jurisdictions that are evolving at different speeds, with overlapping but non-identical disclosure requirements that ultimately need to be translated into a single, coherent view of performance. What may appear manageable at the level of an individual regulation becomes significantly more complex when considered across the full landscape.

CSRD Timelines Are Taking Shape. What 2026 Actually Represents.

For companies not yet in scope, or for those who may never formally report but will still be asked to respond to CSRD-aligned expectations from customers across the value chain, 2026 still has relevance. As reporting expands across industries and regions, expectations begin to move ahead of formal requirements. Requests for information, alignment with frameworks, and exposure to CSRD-style disclosures often arrive before the regulation itself.

Product-Level Carbon Accounting Is Coming. Most Companies Aren’t Ready.

A recent initiative between ISO and the Greenhouse Gas Protocol to develop a product-level greenhouse gas accounting standard signals where reporting is headed next.

Scope 3 Is Getting More Specific. That Changes Supplier Relationships.

Estimates have been accepted. Proxies have been used. Categories have been excluded with qualitative justification. The emphasis has been on directional accuracy rather than precision, but that model is beginning to change.

Sustainability Reporting Is Becoming Standardized. That’s Why Communication Still Matters.

As sustainability reporting becomes more structured, many companies are asking a version of the same question: If disclosures are increasingly standardized, what is left to communicate?

Sustainability in Manufacturing Isn’t a Messaging Problem. It’s a System Problem.

In corporate sustainability, there is a natural pull toward what can be seen. Reports. Scores. Commitments. Certifications. But beneath that visible layer sits something far more consequential, and far less developed: the system that produces the data in the first place.

ESG Platforms Won’t Solve Your Reporting Problem

For companies facing upcoming requirements—whether under CSRD, California climate laws, or investor-driven disclosures—the appeal is clear. In practice, however, many organizations find that implementing an ESG platform does not resolve the underlying problem. It simply organizes it.

Where Climate andSustainability Risk Actually Lives

For much of the past decade, corporate sustainability has been framed through the language of ambition. But something quieter has been happening beneath that narrative.

CSRD Omnibus: A More Useful Way to View the Delay

Much of the early reaction to the CSRD delay has focused on what companies may no longer be required to report, at least in the near term. That perspective, while understandable, risks missing the more meaningful implication of the moment.

Sustainability and the Shift to Operational Reality

2026 is emerging as a year defined less by new frameworks and more by rising expectations. Companies are no longer judged on whether they acknowledge sustainability, but on whether their actions stand up to scrutiny.

Supply Chain Sustainability: From “In Vogue” to Requisite

In the collective imagination of corporate sustainability leaders and consumers alike, “sustainability” often evokes greener materials, ethical labor practices, and circular design. But beneath those admirable ambitions lies a more terrestrial, and often overlooked, truth: sustainability isn’t just an ethos. It’s data. It’s process. And ultimately, it’s a supply chain challenge rooted in accountability.

Why Emissions Data Is Becoming Non-Negotiable for Procurement

When more than 270 major buyers request environmental data from 45,000 suppliers through the CDP Supply Chain program, that’s more than a headline — it’s a market signal. It tells us that emissions data, climate strategies, and credible transition plans aren’t just “nice to have” anymore; they are increasingly material in supply-chain relationships and purchasing decisions.

Making Sense of EU Sustainability Rules in a Moment of “Simplification”

Across the EU, policymakers are adjusting major sustainability directives like CSRD and CSDDD to respond to concerns about complexity and implementation. Thresholds are shifting. Timelines are being fine-tuned. And depending on who you ask, the changes sound like a sigh of relief.It All Begins Here

California’s Climate Disclosure Laws: A New Baseline

California has effectively shifted climate disclosure from a voluntary commitment to an operational expectation. With SB 253 and SB 261, the state has drawn a line around what credible climate transparency looks like, and companies with a footprint in California now have a clearer view of what the coming years will require.It All Begins Here

Corporate Sustainability: The Business Case, Rebuilt

For the last few years, the public conversation has swung between extremes — declarations that ESG is collapsing, predictions that sustainability is losing relevance, and arguments that companies are abandoning their commitments. But when you step inside actual organizations, the atmosphere feels very different. What’s happening is less a retreat and more a recalibration. Pressure from regulators, investors, and customers is pushing companies away from vague ambition and toward initiatives that directly improve financial performance, operational resilience, and competitiveness.It All Begins Here